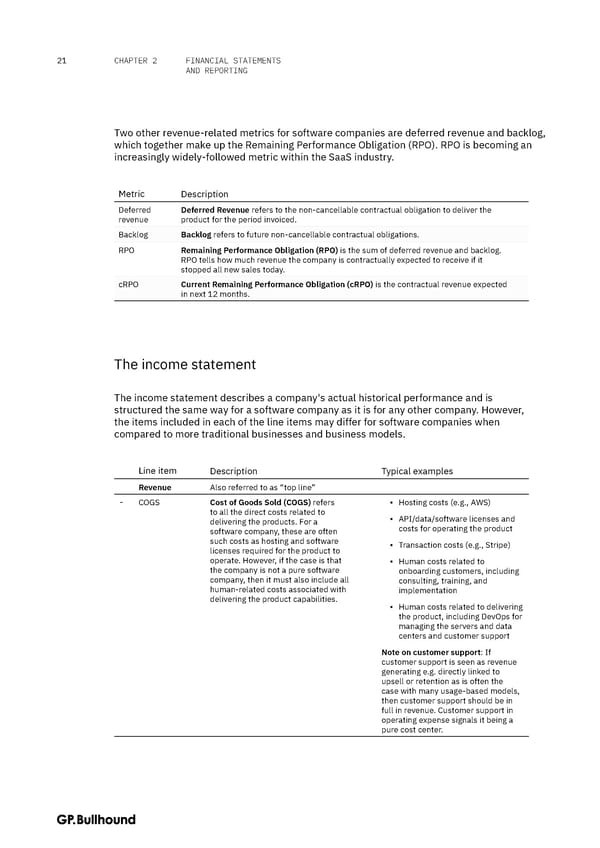

FINANCIAL STATEMENTS 21 CHAPTER 2 AND REPORTING Two other revenue-related metrics for software companies are deferred revenue and backlog, which together make up the Remaining Performance Obligation (RPO). RPO is becoming an increasingly widely-followed metric within the SaaS industry. Metric Description Deferred Deferred Revenue refers to the non-cancellable contractual obligation to deliver the revenue product for the period invoiced. Backlog Backlog refers to future non-cancellable contractual obligations. RPO Remaining Performance Obligation (RPO) is the sum of deferred revenue and backlog. RPO tells how much revenue the company is contractually expected to receive if it stopped all new sales today. cRPO Current Remaining Performance Obligation (cRPO) is the contractual revenue expected in next 12 months. The income statement The income statement describes a company's actual historical performance and is structured the same way for a software company as it is for any other company. However, the items included in each of the line items may differ for software companies when compared to more traditional businesses and business models. Line item Description Typical examples Revenue Also referred to as “top line” - COGS Cost of Goods Sold (COGS) refers ▪ Hosting costs (e.g., AWS) to all the direct costs related to ▪ API/data/software licenses and delivering the products. For a costs for operating the product software company, these are often such costs as hosting and software ▪ Transaction costs (e.g., Stripe) licenses required for the product to operate. However, if the case is that ▪ Human costs related to the company is not a pure software onboarding customers, including company, then it must also include all consulting, training, and human-related costs associated with implementation delivering the product capabilities. ▪ Human costs related to delivering the product, including DevOps for managing the servers and data centers and customer support Note on customer support: If customer support is seen as revenue generating e.g. directly linked to upsell or retention as is often the case with many usage-based models, then customer support should be in full in revenue. Customer support in operating expense signals it being a pure cost center.

The CFO Handbook | GP Bullhound Page 20 Page 22

The CFO Handbook | GP Bullhound Page 20 Page 22